.png)

-

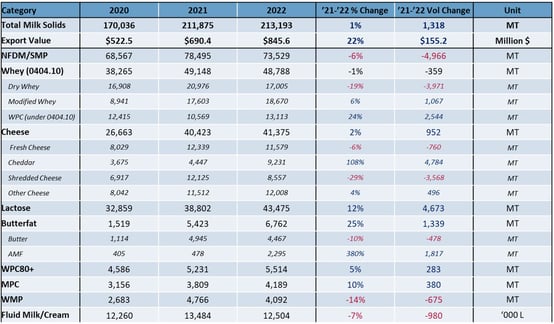

Export volume (milk solids equivalent) ekes out a 1% increase over the previous year with solid performances from multiple product sectors overcoming a 6% drop in NFDM/SMP.

U.S. dairy exports (milk solids equivalent, or MSE) grew 1% in April, setting a new volume record for the month. While the increase was modest, it marked the first year-over-year MSE gain of 2022 and built on a very strong March performance.

April was only the fifth time U.S. dairy exports topped 200,000 MT MSE—the others being March 2022 and March-May 2021. The past two months are encouraging, given that they came in the face of ongoing supply chain challenges, COVID lockdowns depressing Chinese demand, and rampant global inflation.

Year-over-year U.S. export value soared 22% to $845.6 million, second only to March 2022 for highest monthly U.S. export value.

Month of Performance: April

More data and graphs from April’s trade data can be found here.

On a straight volume basis, U.S. cheese exports grew 2% to 41,375 MT in April—only the third time they’ve exceeded 40,000 MT in a single month. Total butterfat exports grew 25% to 6,762 MT. However, that increase was attributable to a nearly five-fold increase in AMF shipments. Year-over-year U.S. butter exports fell for the first time in 17 months, dropping 10% to 4,476 MT.

U.S. lactose exports in April rose 12% to 43,475 MT. Whey product shipments were down 0.1% to 54,302 MT, although that was due wholly to a 19% decline in sweet whey (see below for more on whey).

Outside of sweet whey, the biggest U.S. dairy export decline in April came from NFDM/SMP. Volume fell 6% to 73,529 MT. As in March, U.S. suppliers were unable to duplicate last year’s spike in sales to the Middle East/North Africa (MENA). U.S. NFDM/SMP exports to the region fell 90% (-8,080 MT) compared to April 2021 as limited available supplies focused on Mexico and Southeast Asia.

On the NFDM/SMP plus side, U.S. April shipments to Southeast Asia grew 30% (+7,570 MT), aided by competitive U.S. pricing and slight improvements in U.S. port and shipping operations.

Here’s a closer look at two of April’s main developments:

U.S. cheese shines again

Cheese continues to be the U.S. export star in 2022. After shipping a record 41,693 MT of cheese in March, U.S. suppliers repeated the performance in April with 41,375 MT in exports. It was the first time the United States ever exported more than 40,000 MT in two consecutive months.Furthermore, given only 30 days in April, it was technically a second consecutive record: per-day volume in March was 1,345 MT; per-day volume in April was 1,379 MT.

Central America led growth in April (+40%, +1,189 MT) but volume gains were geographically widespread. April U.S. cheese shipments to Mexico rose 8% (+785 MT); exports to the Caribbean soared 56% (+763 MT); volume to Japan jumped 17% (+738 MT); and exports to the Middle East/North Africa rose 18% (+421 MT).

The gains were more than enough to offset year-over-year shortfalls to Australia, Korea, China and South America.

New U.S. cheddar capacity is helping to fuel the gains. Year-over-year U.S. cheddar exports more than doubled in April to 9,231 MT, with a big portion destined for Japan (likely for further processing). April U.S. cheddar shipments to Japan soared 271% to 3,409 MT.

International cheddar prices continue to favor U.S.-origin product. Even with this week’s dip in Global Dairy Trade cheddar prices and even with CME block cheddar sitting $2.28/lb. (US$5,026/MT) as of Tuesday, U.S. cheddar continues to enjoy a significant price advantage over competitors, suggesting further solid numbers could be in the offing.

Whey hangs tough

Reduced Chinese demand for sweet whey continues to undermine overall U.S. whey exports.Overall U.S. whey export volume was virtually identical to April 2021, despite a 43% decline (-4,234 MT) in shipments of sweet whey to China. U.S. sweet whey exports to all other markets grew 2% (+263 MT). And U.S. shipments of all other whey products (modified whey, WPC and WPC80+) to all markets grew 12% (+3,895 MT).

WPC80+ continued to rebound in April. After five consecutive months of year-over-year shortfalls dating back to October 2021, U.S. suppliers posted two straight year-over-year gains in March (+2%) and April (+5%).

As in cheese, WPC80+ demand was widespread geographically, led by South Korea (+152%, +399 MT), South America (+155%, +360 MT) and the UK (+83%, +284 MT).

Year-over-year U.S. WPC (less than 80% protein) exports grew 24% (+2,417 MT) in April while modified whey (primarily permeate) increased 6% (+1,035 MT). Positive demand from Asia helped drive both categories. U.S. WPC and modified whey shipments to Southeast Asia rose a combined 66% (+3,150 MT), exports to China grew 9% (+1,373 MT) and volume to South Korea increased 168% (+1,048 MT, all of it modified whey).

With no expectations for Chinese sweet whey demand to rebound in the short term, the focus moving forward will remain on other sweet whey markets and the rest of the whey complex continuing to pick up the slack.

Learn more about global dairy markets:

-

U.S. dairy exports finished Q1 strong, as value soared and volume nearly matched 2021 record

-

February butter, cheese exports help mitigate declines in milk powder, whey

-

Dairy export value keeps climbing in January even as supply constrains volume

-

U.S. dairy exports set multiple records in 2021

Subscribe to the U.S. Dairy Exporter Blog

The U.S. Dairy Export Council fosters collaborative industry partnerships with processors, trading companies and others to enhance global demand for U.S. dairy products and ingredients. USDEC is primarily supported by Dairy Management Inc. through the dairy farmer checkoff. How to republish this post.

-