.png)

-

Challenged low-protein whey exports disguised stabilization across rest of the portfolio.

As we’ve discussed in past trade data analyses, global dairy markets remain in a funk. Economic challenges in Asia combined with increased competition from Europe and New Zealand continued to limit U.S. dairy export growth in July. Positively, in most dairy products, declines seen in the second quarter did lessen or even switch to growth.

Source: USDEC, USDA

Source: USDEC, USDAFor more detailed information, as well as interactive charts and data, visit USDEC's Data Hub

NFDM/SMP exports grew for a second straight month, albeit slightly at +3% (+1,783 MT) year-over-year (YOY), almost entirely thanks to robust purchasing from Mexico (+14%, +3,529 MT). Positively, cheese exports, after a challenging second quarter, were roughly flat compared to July 2022 (-1%, -433 MT), thanks to a rebound in sales to Japan and continued growth to Latin America. Still, growth was limited as, sales to Korea and Southeast Asia still faced challenges from demand and competitors selling at lower prices. Similarly, WPC80+ and lactose shipments were effectively flat (-1%, -65 MT; and -2%, -884 MT respectively), though there remains wide variation in performance across markets.

By contrast, with most export products holding steady in July, low-protein whey exports (under the HS code 0404.10) pulled back sharply (-40%, -22,092 MT). In fact, nearly all of July’s overall decline came from weaker low-protein whey shipments. On a milk solids equivalent basis (MSE), export volume declined by 12% (-24,272 MT MSE). Surprisingly, that 12% decline is still a modest improvement compared to the 17% decline in the second quarter. This was despite low-protein whey shipments posting the lowest monthly export volume since 2019, when U.S. whey exporters faced African Swine Fever and retaliatory tariffs on shipments to China.

So, what drove the sharp turn in low-protein whey exports?

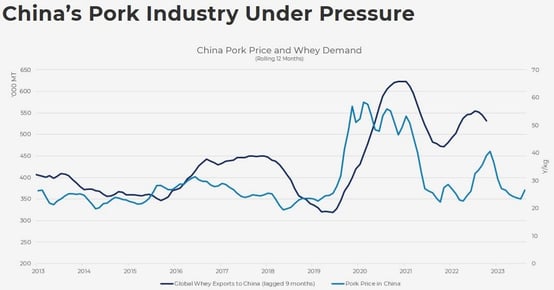

As we noted in previous releases, China is the primary driver of the decline. U.S. low-protein whey exports to the country dropped 21% (-32,898 MT) year-to-date (YTD) and that decline continued in July with exports falling 46% (-12,125 MT) to the lowest monthly level in 18 months.

The fall in whey exports to China largely reflects weaker demand in the feed sector. Chinese pork prices declined sharply earlier in the year, limiting increases in pork production and therefore whey needs. Pork prices are an effective leading indicator for Chinese low-protein whey for feed demand as it signals expansion incentives for local pork producers–

Positively, pork prices have increased 15% from ¥23.65/kg in late July to ¥27.26/kg today. We believe the increase thus far has primarily been driven by lower pork supply rather than increased consumer demand. Additionally, we anticipate a modest seasonal increase in pork consumption in the back half of the year. That improved demand amidst a tighter pork supply should incentivize pork production expansion in China, which should support low-protein whey export recovery towards the end of 2023 and into 2024.

Source: USDEC, Trade Data Monitor, Ministry of Agriculture

Source: USDEC, Trade Data Monitor, Ministry of AgricultureStill, concerns around China’s economy continue to cast doubt on overall consumption within the country – both for pork and dairy. While we anticipate a demand recovery later this year, it is far from certain that China’s demand volatility will stabilize.

Other Relevant Datapoints from July’s Trade Data

- Improved price competitiveness helped support U.S. cheese exports in July. U.S. cheese shipments to Japan had their strongest month of the year, climbing 29% (+935 MT). Similarly, exports to Chile, China and Australia all improved. Even Korea, where cheese exports still lagged 2022 volumes for the month of July by 23% (-1,234 MT), the volume was still notably stronger than the first half of the year (-47% through June). Looking ahead, this improvement in exports should continue in August data, but Q4 cheese exports still face headwinds with lower European and Oceania prices.

- The only cheese category to show growth remains grated/powdered cheese. Shipments of grated/powdered cheese (which is primarily mozzarella) are up 38% YTD (+21,103 MT) with month-of exports even better (+52%, +4,259 MT). While Colby and blue cheese did climb, the increase was negligible (+29 MT and +10 MT, respectively). We’ve seen shredded exports climb to many markets, but Mexico has been the clear engine of growth (+138%, +21,103 MT YTD). Tighter milk production in the U.S. keeping domestic prices elevated above global levels and slower mozzarella production may slow this rapid growth of shredded varieties as we move later in the year.

- WPC80+ exports improved in critical emerging markets even as Japan’s demand slowed. U.S. shipments of high-protein whey continued to excel in Brazil as sports nutrition use has taken off (+67%, +236 MT in July; +108%, +2,312 MT YTD). China, too, showed sizeable growth again in July (+17%, +194 MT for the month; +38%, +2,187 MT). Unfortunately, trade to Japan slowed (-26%, -278 MT), even as YTD shipments remain positive (+6%, +451 MT). Looking ahead, even as WPC80 and WPI prices have tightened of late, they remain within a historically normal range, which should maintain international demand growth and production innovation featuring dairy proteins through the end of the year.

- For the second month in a row, U.S. NFDM/SMP exports to Southeast Asia (SEA) held close to flat. U.S. NFDM/SMP dropped just 45 MT to the region. This is a marked improvement from earlier this year with Vietnam in particular showing significant growth for the month (+206%, +2,333 MT). Still, much of this stabilization is due to weaker year-over-year comparisons as June 2022 was when NFDM/SMP shipments to the region first declined sharply. Optimistically, economic recovery and more favorable comparisons should support improved exports to SEA later in the year, but competition remains fierce.

- Butter shipments fell sharply, largely due to sales to Bahrain going to effectively zero. U.S. butter exports to Bahrain fell by 99.7%, dropping from 2,083 MT in July 2022 to just 7 MT in July 2023. By comparison, aggregate butter exports declined by 61% (-3,730 MT) as U.S. prices diverged from the global prices. U.S. butter prices remain above world levels due to strong domestic sales and slower milk production, which is likely to limit butter exports moving forward.

Learn more about global dairy markets:

-

Dairy exports still challenged by global headwinds in June; What does the second half hold?

-

U.S. dairy exports lagged in May as global headwinds persist

-

Weaker demand and increased competition dent U.S. dairy exports in April

Subscribe to the U.S. Dairy Exporter Blog

The U.S. Dairy Export Council fosters collaborative industry partnerships with processors, trading companies and others to enhance global demand for U.S. dairy products and ingredients. USDEC is primarily supported by Dairy Management Inc. through the dairy farmer checkoff. How to republish this post.