.png)

-

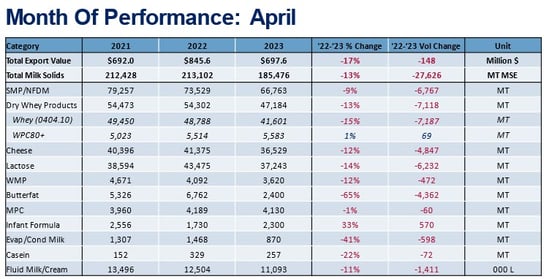

U.S. dairy exports declined by 13% in milk solids equivalent compared to the same month in 2022.

In milk solids equivalent (MSE) terms, April U.S. dairy exports had their worst year-over-year decline in exactly four years. The softness in April exports impacted virtually all the major product categories. Cheese, nonfat dry milk/skim milk powder (NFDM/SMP), low-protein whey, lactose, butterfat, whole milk powder (WMP) and fluid milk/cream all lagged prior-year levels. Of the major products only WPC80+ rose and even that was only by 1%.

In total, the 13% drop in April shipments pulled year-to-date export performance down to -0.3% MSE. Value took an even greater hit, falling 17%, as the recent downturn in dairy product prices is being reflected in the data. Year-to-date value was down 3% through April.

Visit USDEC’s Data Hub for more detailed information

While we anticipated weaker export performance to show up in the data in Q2, particularly in cheese, the scale of the pullback and the variety of products impacted is a surprise.

As we have stated many times, we always caution against over-emphasizing a single month’s worth of data. However, it’s still worth answering the questions of 1) what drove this sharp turn in export performance after several years of consistent growth, and 2) how long should we expect this downturn to persist?

What drove April’s downturn?

At its simplest, global dairy demand has weakened in 2023 at the same time that competition has increased from Europe and New Zealand.

On the demand side, China remains the biggest drag on the global market. Last year, global trade to the largest dairy import market dropped by 22%. This year, while imports have stabilized, they remain subdued, growing by just 2% in the first quarter as a large portion of WMP and fluid milk imports have been displaced by increased domestic production. More recently, weaker margins for pork producers in China have dampened the country’s appetite for whey for feed, which directly impacts U.S. exports.

In addition to the direct impact on U.S. exports, continued weakness in China’s import demand has also sharply increased competition from New Zealand in other key U.S. markets (Southeast Asia, Japan) and products (cheese, SMP), as the Oceania exporter pivoted away from WMP to China. To illustrate this, despite New Zealand production and exports declining in 2022, the decline in China’s WMP purchases effectively increased supply available to the rest of the world by 15% in milk solids equivalent.

However, the challenges in the international environment are not limited to China and New Zealand. Inflation and economic headwinds have dampened consumer demand globally with particularly severe impacts on developing markets in Asia and Africa. Reflecting this weaker demand, U.S. sales to Southeast Asia – still the United States’ second largest market by volume – lagged 2022 volumes by 19% through April.

Compounding all of this, European milk production picked up sharply late last year (+1.2% year-over-year from October 2022 to March 2023) as weather improved and record high milk prices (that persisted even after product prices eased) incentivized additional production. With weak demand within the EU, the surge in milk production was directed towards gouda and mozzarella as well as butter and SMP, leading to a sharp drop in European product prices, effectively undercutting U.S. exports in many key markets.

Expectations moving forward

Clearly, there are headwinds to U.S. dairy exports. Indeed, we’ve highlighted the challenges U.S. dairy exports would face this year for several months. But was April just a singular blip or should we expect further declines?

We expect the next several months of trade data will show similar results, particularly on shipments to Asia, where competition has been particularly fierce and the demand headwinds the strongest.

But as we look towards the later part of the year, we’re optimistic exports will return to growth. Latin America is expected to remain a bright spot for U.S. dairy exports as shipments to Mexico – even in April – remained positive. Additionally, U.S. cheese prices have returned to parity compared to European counterparts which should support a rally in Q3 and Q4 cheese exports to Asia. On top of this, weaker farmgate milk prices within the EU are liable to slow down the bloc’s milk production growth, which in turn should lend support to the market and open opportunities for U.S. exporters again on the ingredient side.

Still, plenty of questions remain on demand in the short-term, particularly in China, Southeast Asia and North Africa. But even so, the U.S. remains well placed to weather the current storm and seize long-term growth opportunities around the world.

Learn more about global dairy markets:

-

U.S. dairy exports dip for first time in a year

-

U.S. dairy exports eke out another volume increase in February

-

U.S. dairy exports start strong in 2023

-

U.S. dairy exports finished record 2022 on a high note

Subscribe to the U.S. Dairy Exporter Blog

The U.S. Dairy Export Council fosters collaborative industry partnerships with processors, trading companies and others to enhance global demand for U.S. dairy products and ingredients. USDEC is primarily supported by Dairy Management Inc. through the dairy farmer checkoff. How to republish this post.

-