.png)

-

U.S. dairy exports rise 5% (milk solids equivalent), driven by whey and lactose, with a little help from butter and cheese.

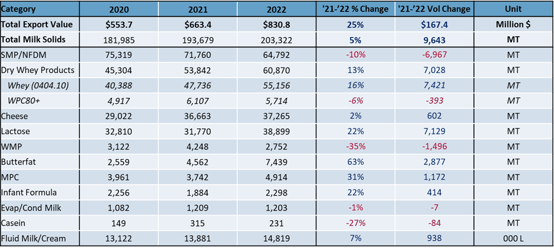

U.S. dairy suppliers posted another strong sales increase in July, with volume up 5% on a milk solids equivalent (MSE) basis compared to last year. Year to date through July, U.S. exports MSE were up 3% over the first seven months of 2021.

U.S. cheese exports continued to expand in July (+2%, +602 MT), albeit at a lower growth rate than we’ve seen throughout most of this year. The bigger drivers for the month were whey and lactose.

Whey exports grew 13% (+7,028 MT) in July with strong increases to almost all major trading partners. U.S. whey exports to China and Southeast Asia (SEA) were particularly good, up 16% (+3,596 MT) and 21% (+2,132 MT), respectively.

Lactose exports jumped 22% (+7,129 MT) in July with strong growth to China (+48%, +3,326 MT) and New Zealand (+78%, +2,419 MT). Butterfat trade also saw gains in July with exports up 63% (+2,877 MT).

U.S. NFDM/SMP continued its downtrend in July, falling 10% (-6,967 MT) vs. the previous year, with weak exports to China, the Middle East/North Africa and Mexico. Ongoing U.S. supply limitations continue to contribute to the shortfall. Year-to-date U.S. NFDM/SMP production is down 9% (-67,540 MT).

Overall, July’s growth in exports showcases U.S. exporter ability to meet the growing global demand in a challenging production and logistics environment.

Let’s dive a bit more into why U.S. exports performed so well, particularly in whey and in trade with SEA.

U.S. Exports: July

For detailed data and charts, check out USDEC’s Data Hub

Whey rises for third straight month

Global demand for U.S. whey continues to recover. Year-over-year U.S. whey exports jumped 13% in July (+7,028 MT), the third straight monthly gain.

For the three-month period of May-July, U.S. whey exports were up 12% (+19,485 MT). In the seven months prior (October 2021 through April 2022), U.S. whey shipments declined 7% (-26,979 MT). Six of those seven months posted year-over-year declines.

Previous USDEC analyses have touched on the reasons for that weakness: supply chain congestion, reduced demand from China (due to a slowdown in that country’s pig sector, a major buyer of U.S. whey for feed) and a spike in U.S. dry whey prices that started last fall and carried through the beginning of 2022.

Improvement at West Coast ports, the moderation of U.S. whey prices and the recovery of China’s pig sector have helped lift demand across all geographies. China led U.S. buying in July, with year-over-year volume up 13% (+3,118 MT). But U.S. suppliers saw widespread whey export gains: Southeast Asia +22% (+2,225 MT); Canada +51% (+1,685 MT); South America +123% (+1,307 MT); and Japan +47% (+860 MT).

In contrast to the overall U.S. whey rebound, U.S. high-value WPC80+ continues to lag previous-year performance. U.S. WPC80+ exports fell 6% in July (-643 MT), right in line with their year-to-date decline of 6% (-2,285 MT). But the decline has been concentrated in two countries—China and the UK—and that remained the case in July.

Year-over-year U.S. WPC80+ shipments to China fell 30% in July (-489 MT) while exports to the UK dropped 80% (-468 MT). Year-to-date through July, U.S. WPC80+ to China was down 45% (-4,758 MT) and volume to the UK was down 63% (-2,286 MT).

Subtract China and the UK from the equation and U.S. WPC80+ exports were up 19% in the first seven months of 2022, driven by significant increase in shipments to Japan (+2,854 MT) and South Korea (+1,266 MT).

Widespread growth in exports to Southeast Asia

Southeast Asia was a high point for U.S. dairy exports this month. Exports to the region in July were up 34% on a value basis and 6% based on volume—helped by record shipments of cheese along with strong growth in whey products and NFDM/SMP. Easing port congestion also helped maintain a steady flow of product.

Cheese exports to Southeast Asia set a new high for the month of July, up 9% (+217 MT) from a year earlier. Driving the gains: shipments of cheddar cheese more than tripled prior-year levels (+224%, +1,166 MT), which offset some weakness in other cheese categories.

Exports of whey products to Southeast Asia continued to recover from the 2021 slowdown and increased by double-digits (+21%, +2,185 MT) for the 12th straight month.

Meanwhile, NFDM/SMP exports to Southeast Asia have yet to best the record shipments that occurred in 2020, but were 5% above year-ago levels in July. WPC80+ exports managed to increase by 20% (+54 MT) versus July 2021, but lagged July 2020 levels. After slowing in the fourth quarter of last year, WPC80+ exports exceeded prior-year levels in February and have delivered year-on-year increases for six consecutive months.

-Sep-07-2022-07-12-21-72-PM.jpg?width=554&name=Chart2%20(2)-Sep-07-2022-07-12-21-72-PM.jpg)

Learn more about global dairy markets:

-

U.S. dairy exports soar in June, climbing 9%

-

U.S. dairy export value surpassed $900 million in May as cheese volume soared

-

U.S. dairy exports post record April

-

U.S. dairy exports finished Q1 strong, as value soared and volume nearly matched 2021 record

-

U.S. dairy exports set multiple records in 2021

Subscribe to the U.S. Dairy Exporter Blog

The U.S. Dairy Export Council fosters collaborative industry partnerships with processors, trading companies and others to enhance global demand for U.S. dairy products and ingredients. USDEC is primarily supported by Dairy Management Inc. through the dairy farmer checkoff. How to republish this post.

-