.png)

-

Solid month for U.S. cheese, WPC80+ exports unable to offset NFDM/SMP and low-protein whey declines.

Despite record shipments of WPC80+ and a rebound in U.S. cheese exports, year-over-year U.S. dairy exports (milk solids equivalent or MSE) fell 12% in September. It was the eighth consecutive decline, dating back to February 2023.

September export value fell 25% to $603 million, the lowest monthly total since January 2022.

Trends that have been keeping overall U.S. exports in check for most of the year remain largely unchanged. U.S. suppliers continue to face strong demand headwinds from tepid global economic growth, elevated inflation and, in the case of low-protein whey, China’s struggling pork sector (though that reportedly has improved of late). While global milk supply growth has slowed, competition from New Zealand and the EU remains tougher than it has been in recent years.

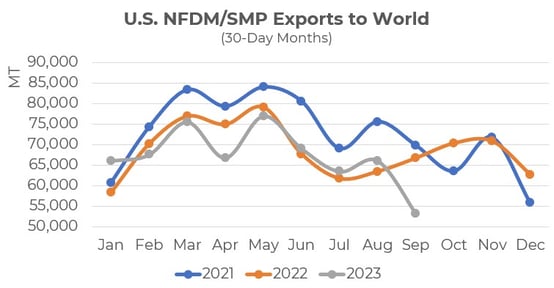

U.S. nonfat dry milk/skim milk powder (NFDM/SMP) exports had their worst month of 2023, falling 20% to 53,256 MT (-13,411 MT). Year-over-year U.S. shipments to Mexico declined for the first time in more than a year (-16%, -5,273 MT). And the nascent recovery in U.S. NFDM/SMP exports to Southeast Asia (+3% for the three-month period of June-August) ended abruptly in September, with year-over-year volume falling 38% (-7,314 MT).

China continued to drag down U.S. low-protein whey sales. U.S. whey shipments to China (0404.10) fell 39% (-11,427 MT), with across-the-board double-digit declines in dry, whey protein concentrate (less than 80%) and modified whey and permeate. U.S. suppliers also saw smaller declines to Mexico (-24%, -928 MT) and Canada (-28%, -1,172 MT).

Gratefully, several positive storylines have emerged in recent months and continued into September, particularly on the higher-value products.

Global cheese demand has proven surprisingly resilient internationally, buoyed by the ongoing post-pandemic recovery in the foodservice sector and Mexico’s robust consumption. Year-over-year U.S. cheese exports rose 4% (+1,531 MT) in September. Shipments to Mexico remained on record pace, jumping 26% (+2,524 MT) and U.S. cheese sales to China more than quadrupled (+1,502 MT). U.S. suppliers also posted strong gains to Southeast Asia (+54%, +543 MT), Central America (+10%, +310 MT) and the Caribbean (+9%, +154 MT).

On top of the positive cheese story, the increasingly global nutritional appeal of high-protein foods and beverages, coupled with favorable pricing of high-protein whey, drove WPC80+ demand to an all-time high. The U.S. shipped 7,356 MT of WPC80+ in September, a 40% increase (+2,118 MT) over the previous year. It was the first time U.S. shipments cleared the 7,000-MT mark—and in a 30-day month no less. U.S. WPC80+ exports to Japan—our top market—more than doubled (+1,078 MT) while volume to China more than tripled (+1,070 MT).

Through three-quarters, on an MSE basis, U.S. dairy exports were down 7.5% compared to the previous year. Value through three quarters was $6.23 billion, down 15%.

For a deeper dive into the key product categories of cheese and NFDM/SMP, see below.

.png?width=554&height=302&name=Chart101%20(2176%20x%201500%20px).png)

For more detailed information, as well as interactive charts and data, visit USDEC's Data Hub

Q3 rebound in cheese exports

After a rough second quarter, U.S. cheese exports returned to neutral in Q3 – decreasing just 16 metric tons compared to the 17% (-20,986 MT) decline in Q2. Mexico remained the largest positive contributor to U.S. cheese exports in Q3, increasing 15% for the quarter and 26% in the month of September thanks to robust consumer demand and a strong peso. Shredded cheese, in particular, has been the cheese of choice for Mexican buyers, more than doubling in 2023.

Still, the major change in Q3 was the improvement in several markets other than Mexico. U.S. cheese exports to Japan went from -29% (-4,358 MT) in Q2 to +15% in Q3 (+1,570 MT); Australia went from +3% (181 MT) to +16% (+878 MT); and sales to Central America jumped 23% (+2,060 MT) compared to a 17% drop in Q2 (-2,350 MT).

Naturally, not every market was positive. Sales to Korea continue to be hammered by weak demand and stiff competition from European suppliers, falling by more than a third in Q3 (-35%, -6,845 MT). Sales to the Middle East/North Africa (MENA) dropped by 41% in Q3 (-3,066 MT) for similar reasons. This contrast between Korea and MENA and most other U.S. markets resulted in cheese trade holding roughly neutral, which is still a marked improvement from Q2 and is being compared against a record 2022.

So, what drove the improvement in Q3 after the challenging second quarter?

Certainly, price was a major determinant. As we said in plenty of past reports, U.S. cheese prices were uncompetitive for late 2022 and the first half of 2023 as European cheese prices dropped precipitously and domestic sales and exports to Mexico helped keep U.S. prices elevated relative to the world market. This naturally led to a sharp drop in Q2, but as U.S. prices declined over the summer and European prices firmed, exports to highly competitive markets like Japan improved.

Fortunately, U.S. cheese prices have improved since the lows of June and July with roughly comparable prices across the major exporters, which should help maintain the stabilization of U.S. cheese exports into the fourth quarter and 2024, provided global demand improves with a (slightly) more optimistic economic outlook.

NFDM/SMP turns downward again in September

U.S. NFDM/SMP exports had almost drawn back to even through the first eight months of 2023, with gains in June, July and August. Volume was 558,407 MT—only 283 MT less than the previous year. However, a 20% year-over-year shortfall in September dug the year-to-date hole a little deeper. U.S. NFDM/SMP exports through the first three quarters were 611,663 MT, a 2% decline from the first three quarters of 2022.

September’s weak performance stems largely from our two largest buyers—Mexico and Southeast Asia—although the reasons behind each market’s decline varied.

U.S. shipments to Southeast Asia fell 38% (-7,314 MT) in September to 11,738 MT. The disappointing result came after U.S. suppliers appeared to be rebounding from a longer-term slump in growth to Southeast Asia. U.S. NFDM/SMP exports to the region rose 3% (+2,034 MT) over the June-August period. While that three-month period compared to a down year in 2022, volume still averaged more than 20,000 MT per month.

The September results marked a significant step down. At 11,738 MT, it was the lowest U.S. monthly volume (30-day months) to the region in six years. While it is true that New Zealand has been channeling more milk to butter/SMP, boosting its export supply, the broader issue overall is slow Southeast Asian demand. New Zealand SMP exports to Southeast Asia fell 34% in September and were down 24% in the third quarter. EU SMP exports to Southeast Asia fell 15% in August (latest available data).

Mexico is a different story. U.S. NFDM/SMP exports to our No. 1 market fell 16% (-5,272 MT) in September. It was the first year-over-year decline since August 2022. But it did not come out of nowhere. U.S. NFDM/SMP exports to Mexico jumped 31% in the first eight months of the year to 286,141 MT—well on their way to a new annual record. While they are still on record pace, the size of the year-over-year gains has been dwindling since May, dropping into the negative in September.

We see a few reasons behind the slowdown in growth, including the build-up in supply, the value of the peso and slowdowns at the U.S.-Mexico border that began worsening in September.

The Mexican peso reached a multi-year high against the U.S. dollar in July, making U.S. powder more affordable. But the peso slowly lost value from July through mid-October, overlapping a rise in U.S. NFDM/SMP prices that began in early August.

Improvements in the peso-U.S. dollar exchange rate since mid-October provide some reasons for optimism on NFDM/SMP shipments to Mexico moving forward, particularly as stalled product is accounted for. But uncertainties remain regarding Southeast Asian demand.

Learn more about global dairy markets:

-

Global headwinds hamper U.S. dairy exports again in August

-

Slow whey demand in China holds back U.S. dairy exports in July

-

Dairy exports still challenged by global headwinds in June; What does the second half hold?

-

U.S. dairy exports lagged in May as global headwinds persist

Subscribe to the U.S. Dairy Exporter Blog

The U.S. Dairy Export Council fosters collaborative industry partnerships with processors, trading companies and others to enhance global demand for U.S. dairy products and ingredients. USDEC is primarily supported by Dairy Management Inc. through the dairy farmer checkoff. How to republish this post.

-