.png)

-

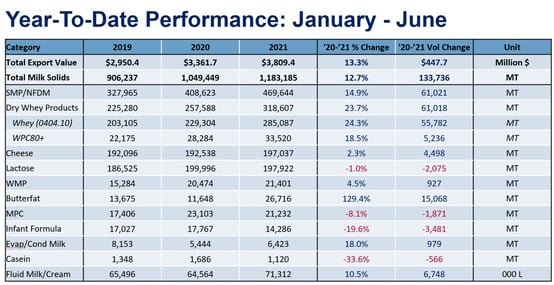

Through June, U.S. dairy exports in 2021 are up 13% in both volume and value compared to 2020.

June export figures align with many of the trends we’ve seen throughout the first six months of 2021: dairy ingredients drove the majority of June’s growth in volume and higher commodity prices pushed value up at an even faster pace.

Total dairy export volume on a milk solids equivalent basis picked up 6% and total export value grew 15% to $670 million. Whey exports grew the most with an additional 6,973 metric tons (MT) shipped out compared to June 2020, a gain of 16% driven by demand from China. Non-fat dry milk/skim milk powder (NFDM/SMP) wasn’t far behind, growing 5,579 MT, a gain of 7%, thanks to recovering demand in Mexico. Cheese exports faltered in the face of strong year-over-year comparisons, declining by 5,031 MT (-13%).

Detailed data and charts can be found here.

For this month’s write-up, we’re going to focus less on June’s data and more on the key dynamics we’ve seen in the first half of 2021 in each of the United States’ major products and how we see these themes playing out in the back half of the year.

NFDM/SMP

-3.jpg?width=554&name=Chart2%20(3)-3.jpg)

Starting with our largest export product, NFDM/SMP, the primary dynamic affecting U.S. export performance remains the congestion at port, particularly in California. Exporters repeatedly dealt with container ships canceling or rolling bookings, lack of equipment, and narrow windows to get the product to port, all of which weighed on U.S. exports to the Asia-Pacific, but particularly NFDM/SMP to Southeast Asia (SEA).

To be clear, delayed product still moved – NFDM/SMP shipments to Southeast Asia are up 1% (+1,133 MT) through the first half of the year – but we believe that plenty of product that has been booked for export has not left U.S.’ shores yet. Additionally, delays outside of the control of U.S. exporters have hampered the U.S.’ ability to maintain market share in the region as European suppliers have been aggressive in pushing greater volumes to the region (+25,257 MT through May).

With logistics congestion slowing U.S. export growth to Southeast Asia, the recovery in demand out of Mexico has been particularly welcome. Total NFDM/SMP exports to Mexico were up 25% year-to-date (+33,288 MT) and were even ahead of 2019 volumes through June. While we attribute some of the strength in Mexico’s demand to drought that is affecting local milk production, the overall gain in imports is still a positive signal for recovering consumer demand within the country.

What does this mean for the rest of 2021?

Well, all signs point to port congestion remaining a headache for U.S. exporters through at least the end of the year. While those delays will act as a headwind and dampen U.S. exports to the Asia-Pacific compared to what they would be without port delays, we still expect strong growth overall in NFDM/SMP exports in the second half.

As mentioned earlier, plenty of milk powder has already been sold to overseas buyers is sitting in a warehouse waiting to be shipped. That product will move – even if it ships two months later than it was supposed to. Additionally, the U.S. milk production outlook in the back half of the year continues to look incredibly robust, which will result in plenty of available supply for export. Finally, U.S. domestic demand for NFDM is expected to remain weak with so much raw milk available; this will also push greater volumes into the export market.

Overall, while there remain plenty of watchouts to this optimistic forecast – the most significant being COVID-19 outbreaks in Southeast Asia – the U.S. should be well placed to grow its NFDM/SMP in the second half of 2021 given limited milk production growth out of Europe and New Zealand’s additional milk fixated on satisfying Chinese demand.

Whey

The story for whey in the first half of the year has been all about demand. Total U.S. whey exports in June grew 16% (+6,973 MT) over June of last year. High-value protein continues to show strong growth as well with WPC80+ June exports up 43% (+1,899 MT) over June of last year.

.jpg?width=554&name=Chart3%20(4).jpg)

This story of steady expansion has characterized the first half of the year. US whey exports are up 24% year-to—date (+66,670 MT) over the same period last year which puts the U.S. on pace to have yet another record year in whey exports.

At the risk of sounding like a broken record, China is fueling the growth. In June, US whey exports to China were up 39% (+7,513 MT) and are up 75% (+66,670 MT) through the first half of this year. As we’ve said many times before, whey for feed has been the key driver for Chinese sweet whey and whey permeate imports as the pork industry consolidates into more commercial operations and continues to rebuild its pig herd following the devastation of African Swine Fever (ASF). The approval for permeate to be used in food has undoubtedly helped as well, but the market remains small at this point. On the high-value side, China’s push to increase its domestic infant formula manufacturing has increased WPC80 demand.

What does this mean for the rest of 2021?

As we look to the second half, the seemingly insatiable demand we saw over the last year has more recently been put into question with the collapse of pork prices in China pinching pig farmers’ margins and signaling to the industry to curb expansion. This seems to have already impacted whey demand as U.S. dry whey prices have fallen from their peak and industry contacts confirm Chinese purchasing has slowed.

Still before we get too pessimistic, that decline in price fails to tell the full story. More recent outbreaks of ASF in China created a frenzy among producers as they sent hogs to market in an attempt to avoid any outbreaks on their operations, which then fueled that price collapse with a glut of supply. The price free-fall has subsided in recent weeks, but prices remain in line with pre-ASF levels. If we remain at these price levels, we are unlikely to see the level of feverish whey demand continue through the back half of this year. However, if prices begin to tick back up, we may see renewed demand growth as pork production margins become more conducive for expansion.

Additionally, while it sometimes seems like it, the whey market is not only about China, particularly when we talk about higher protein whey products. US whey exports to countries other than China showed solid growth through June in face of historically high global prices. U.S. exports to SEA and Korea have also experienced growth with SEA expanding by 2% (1,181 MT) and Korea’s WPC80+ demand surging by 77% (+4,276). Overall, demand is expected to be strong globally for whey in the back half of the year, and while there is risk of a slight pullback from China, we still expect whey exports to be at, or more likely above, where they were in 2020 through the end of year.

Cheese

Compared to the relatively steady growth of NFDM/SMP and whey, U.S. cheese exports have been on a rollercoaster. U.S. cheese exports went from a 10% year-over-year decline in January to a 51% spike in April to a 13% decline in June, with other monthly results somewhere in between. Still, U.S. cheese sales managed positive growth through the first six months and rose a respectable 2.3% to 197,036 MT compared to the previous year.

-2.jpg?width=554&name=Chart4%20(3)-2.jpg)

While many factors are responsible, two stand above the rest:

First, there has been wild fluctuation in year-over-year comparisons. In 2020, cheese export volumes swung from multi-year lows in April to multi-year highs in June as a result of extreme price swings. For instance, June 2020 cheese exports were higher than at any point last year. However, that cheese was exported at $650/MT cheaper than June 2021. Essentially, matching 2020 volumes at current prices was an exceedingly difficult feat.

Second, the stop-start nature of foodservice reopenings around the world as the race between vaccines and variants continues to slog on has resulted in export volumes varying significantly from month to month.

They are not the only factors – economic growth, U.S. shipping issues and other influences continue to affect cheese demand and exports as well – but they are the main drivers.

We’ve seen that translate to major swings in purchasing, with Japan and South Korea being two of the best examples. Through the first four months of 2021, U.S. cheese exports to Japan were up 32% and sales to South Korea were up 29%. Through the first six months, after factoring in May-June numbers, U.S. cheese sales to Japan were up 2% and volume to South Korea was lagging the first six months of 2020 by 5%. A rollercoaster indeed.

What does this mean for the rest of 2021?

On the optimistic side, U.S. cheese prices (while still exhibiting some volatility) remain favorable compared to major competitors, incentivizing international customers to look to the U.S. for cheese. Additionally, U.S. cheese supply should remain plentiful with new capacity and plenty of milk production growth, particularly in the Midwest, expected through 2021. And while nations are tightening foodservice restrictions in the face of the Delta variant, few of the major cheese buyers have so far returned to complete lockdown status.

Still, if you read the half-year reports from major dairy and food suppliers this year, you will see one word repeated frequently: “uncertainty.” For the rest of the year, much of U.S. cheese export performance will depend on pandemic progress.

Overall, we anticipate favorable pricing, good demand and plenty of supply available for export which should result in growth in the second half of the year, but don’t expect the rollercoaster to be over. Third quarter U.S. cheese exports were strong in 2020 and set a challenging bar, while 2020 cheese export volumes in the fourth quarter were some of the worst in years.

To make sense of this uncertainty, be sure to stay tuned for future trade data updates out of USDEC.

Learn more about global dairy markets:-

Dairy exports show few signs of slowing in May

-

U.S. dairy exports maintain momentum in April

-

U.S. dairy exports hit all-time record in March

Subscribe to the U.S. Dairy Exporter Blog

The U.S. Dairy Export Council fosters collaborative industry partnerships with processors, trading companies and others to enhance global demand for U.S. dairy products and ingredients. USDEC is primarily supported by Dairy Management Inc. through the dairy farmer checkoff. How to republish this post.

-