.png)

-

Ingredients drive U.S. dairy exports to a near-record month.

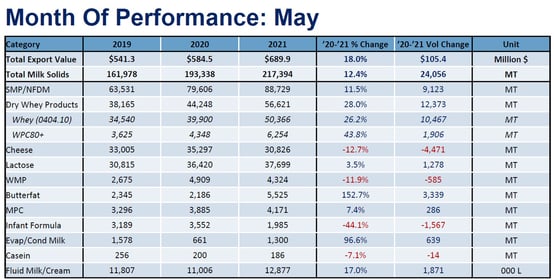

While record cheese exports pushed U.S. exports to record heights daily in April, it was ingredients that drove May volumes to nearly that same record level – with May as the second highest month for most dairy exports shipped in a single month on a daily basis. Compared to May last year, U.S. Dairy export volume in milk solids equivalent grew 13%, with the total value of those shipments 18% higher.

Overall, a surge in non-fat dry milk/skim milk powder (NFDM/SMP) to Mexico and the Middle East/North Africa (MENA) and the continued demand for whey in China were the primary drivers of ingredient export growth. Port issues continued to frustrate U.S. dairy exporters in May, but as we have seen the past few months, U.S. exporters are finding ways to manage the delays at port and address rising freight and trucking rates.

More detailed data and charts can be found here.

Beyond that topline, here are our three main takeaways from the May export data:

NFDM/SMP exports soar

U.S. NFDM/SMP exports jumped 12% (+9,566 MT) to 88,729 MT in May. That’s the most NFDM/SMP the United States has ever shipped in a single month, topping the 86,532 MT exported in March of this year.

Strong global demand and favorable U.S. pricing continue to support U.S. sales. As a result, U.S. NFDM/SMP exports were up 17% to 388,209 MT, well above record annual pace through the first five months.

May gains came in most major markets.

U.S. NFDM/SMP shipments to Mexico grew 28% (+6,752 MT) vs. May 2020. Mexican NFDM/SMP purchasing has ticked up every month since January. Better-than-expected economic growth this year is a significant driver, but drought is likely playing a role as well. Around two-thirds of Mexico is facing drought conditions, and forecasts are calling for the situation to worsen in the coming weeks, causing widespread water shortages and crop damage.

May U.S. NFDM/SMP exports to the MENA region jumped 161% (+5,994 MT), led by Algeria (+3,993 MT). Similarly, sales to China doubled (+2,973 MT). Favorable U.S. pricing and efforts in both regions to diversify supply supported U.S. trade.

U.S. sales to Southeast Asia fell 11%. Gains to Vietnam, Malaysia, Thailand, and Singapore weren’t enough to offset a sharp decline to Indonesia (-46%) and a 14% drop to the Philippines.

Given global demand, U.S. production and stocks, favorable pricing, and the ongoing U.S. shipping backlog, there is strong reason for optimism for continued NFDM/SMP success in the coming months. On top of this, even after the record month, indications are we have more booked product waiting for a ship).

Cheese volumes step back after record April

Of the major export products, cheese was the only U.S. dairy export to take a step back in May. Total volume was down 13% (-4,471 MT). Shipments to Asia-Pacific saw the sharpest pullback. Exports to Korea and Japan fell by 36% each (-3,403 MT and -1,949 MT, respectively), and volumes to Australia dropped by 51% (-1,317 MT). Mexico bucked the trend with a 14% increase in imports (+1,023 MT).

However, before we sound any alarm bells over reduced international demand in Asia, it is worth comparing the market conditions in May 2020 and May 2021. May 2020 came right after historically low cheese prices in April (falling as low as $1/lb.) as the COVID-19 pandemic and foodservice closures hammered U.S. domestic cheese demand. This meant that there was plenty of available cheese for export at very competitive prices in May last year. You can see this in the contrasting export prices as the average unit value of cheese exported in May 2020 was almost 30 cents per pound cheaper than in May 2021. The sharp deterioration of the Mexican peso negated much of the price decline in the U.S., so it was primarily Asia-Pacific customers who bought more U.S. cheese last year.

Contrast last year’s experience with this May: The U.S. economy is opening up rather than shutting down. While U.S. supply was booming this year thanks to new capacity, demand grew alongside it as foodservice establishments replenished pipelines for waves of customers, which also kept prices supported. On top of that, the port issues likely delayed some booked export orders in May.

Yet, today, cheese is more readily available. Supply is still booming and domestic demand has backed off as foodservice pipelines have finished refilling and retail demand slows. With global demand for cheese accelerating as many countries reopen, we remain optimistic that this combination of factors should result in increased U.S. cheese exports in the coming months.

WPC80+ demand growth

U.S. total whey exports in May were up 28% (+12,373 MT) over May of last year. A key driver of the growth has been higher value products. WPC80+ exports were up 44% (+1,906 MT) over May 2020 and up 73% over 2019. During May of last year, gyms were closed, travel was limited, and many consumers were eschewing fitness for comfort foods, leading to a decrease in WPC80+ demand. So it comes as no surprise that as the world reopens and consumers seek healthier products after a sedentary 2020, demand is returning. Equally encouraging is the growth over more “normal” 2019 levels, which illustrates an increased global appetite for WPC80+.

The diversity in the growth of U.S. WPC80+ markets is particularly encouraging as no single market was driving the growth. Exports to China expanded by 342 MT, the United Kingdom by 335 MT, South Korea by 315 MT, and Brazil by 240 MT. Turkey grew from 0 MT in May 2020 to 194 MT. Canada, Japan, Vietnam, and Mexico all grew by more than 100 MT. Of the major markets, only India pulled back, which resulted from non-tariff barriers being erected last year, effectively blocking the U.S. from that market.

Moving forward, the continued reopening of economies and the associated refocus on health and wellness should be a major boost for WPC80+ demand. Additionally, increased cheese capacity coming online in the U.S. paired with the strong growth in milk production bodes well for both WPC80+ production and exports.

Learn more about global dairy markets:-

U.S. dairy exports maintain momentum in April

-

U.S. dairy exports hit all-time record in March

-

U.S. dairy exports surge despite shipping woes

Subscribe to the U.S. Dairy Exporter Blog

The U.S. Dairy Export Council fosters collaborative industry partnerships with processors, trading companies and others to enhance global demand for U.S. dairy products and ingredients. USDEC is primarily supported by Dairy Management Inc. through the dairy farmer checkoff. How to republish this post.

-