.png)

-

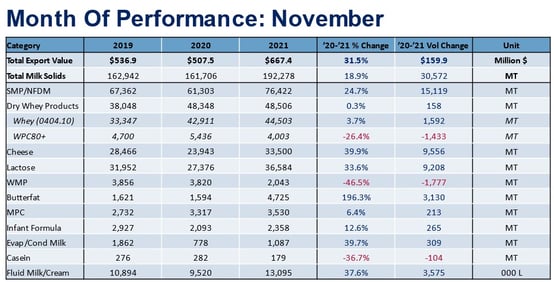

With one month of data to go in 2021, U.S. dairy exports are finishing on a high note.

U.S. dairy exports rebounded sharply in November, climbing 19% in volume (milk solids equivalent) and an astonishing 32% in value compared to the same month in 2020. Nonfat dry milk/skim milk powder (NFDM/SMP) and cheese led the way with growth rates of 25% (+15,119 metric tons, or MT) and 40% (+9,556 MT), respectively.

Through the first 11 months of 2021, U.S. dairy export volume (milk solids equivalent) was up 12% and already surpassed the annual record established in 2020. Additionally, U.S. dairy export value also ran 18% ahead of the same period the previous year, reaching $7.14 billion through November.

More data and graphs from November's trade data can be found here.

NFDM/SMP rebounds – Paul Rogers

For the past three years, we have seen strong October NFDM/SMP shipments followed by weaker Novembers. This year, that pattern reversed.

After shipping 66,862 MT in October (only the second month in 2021 that U.S. volume failed to top 70,000 MT), U.S. NFDM/SMP exports boomeranged to 76,422 MT in November—easily a record for the month.

-Jan-06-2022-08-21-19-82-PM.jpg?width=554&name=Chart2%20(2)-Jan-06-2022-08-21-19-82-PM.jpg)

Gains were broad-based, though clearly led by Southeast Asia. U.S. shipments to Southeast Asia grew 37% (+7,275 MT) year-over-year, driven by significant increases to Vietnam (+292%) and the Philippines (+76%). Backlogged product finally making it to buyers likely contributed to regional volumes in November, but the percentage gain to Southeast Asia also benefitted from a weak November 2020. As a result, the United States shipped only 19,611 MT to Southeast Asia in November 2020—which was the lowest monthly total of the year up until that point (December 2020 dipped to 17,181 MT).

U.S. suppliers also posted significant increases in most major markets beyond Southeast Asia: South America (+37%, +2,834 MT), Mexico (+9%, +2,229 MT), Central America (+196%, +2,024 MT) and China (+27%, +726 MT).

An exponential increase in exports to Honduras—1 MT in 2020 vs. 1,372 MT in 2021—drove the Central America total, while a 45% increase (+2,417 MT) to Colombia (presumably in anticipation of January’s quota opening) lifted South American volumes.

Mirroring the spike to Honduras, U.S. NFDM/SMP shipments to Yemen jumped from 25 MT in November 2020 to 1,325 MT in 2021. Both nations made a rare appearance as top-10 U.S. NFDM/SMP destinations in November.

Global NFDM/SMP demand remains strong. In the months ahead, readers should watch whether the U.S. price advantage with the EU and New Zealand, which has narrowed significantly since September, will affect U.S. performance as we move into the New Year.

Cheese soars – William Loux

U.S. cheese exports have surged in the second half of 2021, placing U.S. cheese exports on pace to finally surpass the annual export record set in 2014. Strong demand from the United States’ major partners and weak production from primary competitors have been crucial to accelerated sales. In November, volumes to Mexico particularly shone with an increase of 65% (+3,539 MT), though the rest of Latin America was not far behind (+46%, +2,313 MT). South Korea (+48%, +1,745 MT) and Australia (+107%, +1,157 MT) also had strong months.

-Jan-06-2022-08-22-15-96-PM.jpg?width=554&name=Chart3%20(2)-Jan-06-2022-08-22-15-96-PM.jpg)

Indeed, the U.S. has seen growth in multiple cheese types as economies rebounded in 2021, tourism returned, and consumers went back to restaurants regularly. However, digging into the data more, we see that cheddar exports, in particular, are having a resurgence. Over the past several years, cheddar production has primarily been geared towards the domestic market, with exports increasing by less than 3% per year since 2015.

However, with expanded capacity in the U.S. and competitive pricing, the amount of cheddar cheese moving overseas has reached its highest point since 2015. Year-to-date cheddar exports have increased by 30%, an increase of more than 10,000 MT. In just the last three months, volumes increased more than 7,000 MT year-over-year. Although from a much smaller base, cheddar cheese exports are growing at the fastest pace of any of the major cheese export categories this year.

-Jan-06-2022-08-22-55-79-PM.jpg?width=554&name=Chart4%20(2)-Jan-06-2022-08-22-55-79-PM.jpg)

Overall, most of that growth is attributable to Japan's increased purchasing of cheddar for further processing. In what is arguably the most competitive cheese import market in the world, U.S. competitors failed to have sufficient product for Japanese buyers and U.S. prices were much more in line with global benchmarks, both of which have enabled the U.S. to gain market share.

Looking ahead, the picture for cheese exports – particularly cheddar – appears favorable in the new year. International cheese demand appears resilient despite renewed COVID outbreaks (as GDT climbed again on Tuesday), U.S. prices remain competitive and, even with tight milk supplies domestically, cheddar cheese plants continue to run at full capacity. All those factors should support further growth in cheese exports in 2022.

And whey holds steady – Stephen Cain

Total whey exports in November were essentially flat (+0.3%, +158 MT) compared to November of last year. Increased exports to Southeast Asia (+26%, +2,249 MT), Japan (+40%, +894 MT), South Korea (+22%, +455 MT), Mexico (+40%, +1,269 MT) and other smaller partners helped offset the strong decline in shipments to China (-24%, -5,245 MT).

For this month, let’s dig into whey protein concentrates (WPC) specifically, as exports were down 18% (-3,233 MT) in November with strong declines from China (-40%, -3,950 MT) and Canada (-12%, -301 MT).

Two factors are likely playing into the lower exports.

First, export prices of U.S. WPC are the highest they’ve been in roughly eight years. November export prices reached $4,576/MT, nearly 60% higher than the average 2020 price of $2,901/MT. These higher prices are pushing buyers to purchase only what they need in the short term.

Second, there is likely less exportable supply available. U.S. production of WPC did grow in October as output reached its highest monthly level since early 2018. Usually, with higher production, exports would be the primary destination for the increased volume. However, strong domestic demand (+6% YTD) has kept the product at home and contributed to an overall decline in WPC inventory of 2% year-over-year. This data tracks with the renewed focus on health and wellness as consumers returned to gyms and pursued healthier lifestyles; both driving higher value protein consumption.

So, while exports of WPC may be down, it is unlikely that reduced international demand is the culprit, but rather high prices and tighter exportable supply slowing export growth.

-Jan-06-2022-08-23-28-31-PM.jpg?width=554&name=Chart5%20(2)-Jan-06-2022-08-23-28-31-PM.jpg)

Learn more about global dairy markets:

-

Cheese, butterfat exports soar in October; milk powder, whey lag

-

Increases across the board keep U.S. dairy exports on pace for another record year

-

Seventh straight month of growth for U.S. dairy exports

-

Cheese and whey drive U.S. dairy exports to 6th straight month of growth

Subscribe to the U.S. Dairy Exporter Blog

The U.S. Dairy Export Council fosters collaborative industry partnerships with processors, trading companies and others to enhance global demand for U.S. dairy products and ingredients. USDEC is primarily supported by Dairy Management Inc. through the dairy farmer checkoff. How to republish this post.

-