.png)

-

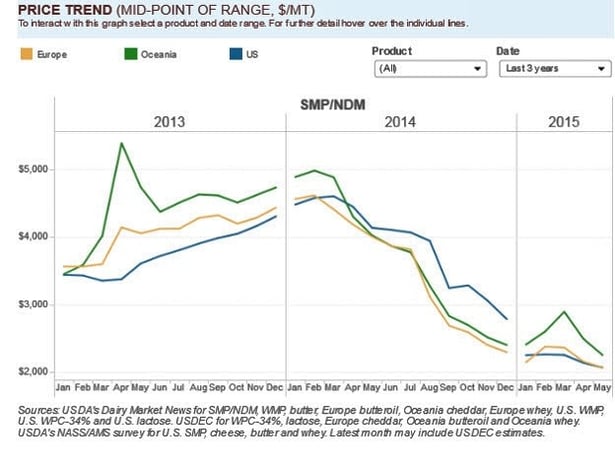

It’s still a buyers’ market as SMP prices approach EU intervention levels.

It’s still a buyers’ market as SMP prices approach EU intervention levels.The world dairy markets are rebalancing slowly, leaving prices at or near six-year lows. Without the large imports from China and Russia seen in previous years, it will take a greater, lengthier contraction in production to clear overhanging supply. In the first quarter, milk production from the five major exporters was up about 0.1 percent vs. prior year. However, China imports of milk powder, cheese, butterfat and whey were down 40 percent and Russia’s imports through February were off 86 percent (not counting trade with Belarus).

Imports from other buyers have increased, but not enough to pick up the slack. Countries boosting purchases of milk powder, cheese, butterfat and whey in early 2015 include: Mexico (+18 percent through February); Japan (+19 percent through March); South Korea (+23 percent through April) and Southeast Asia (+19 percent in January).

Broadly, however, buyers are satisfied with their coverage and feel no urgency to buy ahead in a weak market. Negotiations for the second half of the year are progressing slowly.

With recent declines, skim milk powder prices are near EU intervention levels (1698 euros/ton; $1934/ton). Traders are anticipating product to move into storage soon.

Two upcoming events will help shape near-term market psychology. Traders are waiting for the results of a new Algerian tender, for an estimated 60,000 tons of milk powder for July-October delivery. Also, Fonterra will make its initial projection of 2015/16 payout next week. Most analysts expect a forecasted payout of NZ$5.60 to NZ$5.70.

Other fundamental indicators:

-

EU-28 milk deliveries in the first quarter are estimated at 35.8 million tons, down 0.5 percent from the extraordinary levels of last year. Among key countries in Q1: Ireland -4.3 percent; Netherlands -2.2 percent; Germany -1.7 percent; France -2.7 percent.

-

In the first quarter, New Zealand milk production was down 2.0 percent but this was nearly offset by a 3.7 percent increase from Australia. New Zealand production is winding down for the season.

-

U.S. milk production continues to expand. April output was 8.1 million tons, up 1.7 percent from prior year.

-

In the first quarter, China imported 164,165 tons of WMP, down 50 percent from the exceptional volumes bought last year, though a little bit more than the 2011-13 Q1 average. SMP imports were down 38 percent and whey products were down 10 percent from a year ago.

-

NZX futures continue to reflect bearish sentiments. WMP futures average $2594/ton to December.

-

The GlobalDairyTrade (GDT) Price Index dropped for the fifth event in a row at the May 19 auction, falling 2.2 percent to an average winning price of $2,472/ton. The Index has dropped 27 percent since early March and now sits at its lowest level since August 2009. WMP was down 0.5 percent to an average winning price of $2,390/ton, SMP was off 3.6 percent to $1,992/ton and AMF was down 4.8 percent to $3,337/ton.

The U.S. Dairy Export Council is primarily supported by Dairy Management Inc. through the dairy farmer checkoff that builds on collaborative industry partnerships with processors, trading companies and others to build global demand for U.S. dairy products.

-