.png)

-

Weak demand and increased competition limit U.S. dairy export growth in 2023 to high-protein whey and lactose.

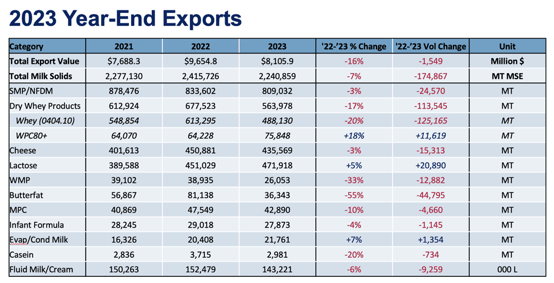

Subdued demand, coupled with increased competition from the EU and New Zealand, translated into a U.S. dairy export decline of 7% in milk solids equivalent terms (MSE) in 2023. The factors complicating U.S. dairy export growth have been consistent most of the year: elevated inflation, disappointing economic growth in key export markets (particularly China), reduced demand for feed whey from China’s struggling pig sector, increased milk output from the EU and New Zealand, and reduced whole milk powder (WMP) purchasing from China causing New Zealand to shift its product mix and redirect exports to key U.S. markets.

U.S. export value finished the year at $8.11 billion. That is the second largest value of all time but down 16% from the record year of 2022 as both volume and prices eased.

U.S. suppliers posted volume gains in only two major product categories in 2023: high-protein whey (WPC80+) and lactose. Full-year U.S. WPC80+ export volume jumped 18% (+11,619 MT) compared to 2022, rising to a record 75,848 MT. Fueled by strong gains in the first quarter, lactose shipments rose 5% (+20,890 MT) to a record 471,918 MT.

But beyond WPC80+ and lactose, positive year-end numbers were nowhere to be seen. Nonfat dry milk/skim milk powder (NFDM/SMP) fell 3% (-24,570 MT); cheese dipped 4% (- 15,313 MT); low-protein whey dropped 20% (-125,165 MT); butterfat slid 44% (-44,795 MT). Milk protein concentrate, fluid milk and cream and whole milk powder fell 10%, 7% and 33%, respectively, for the year. For more detailed information, as well as interactive charts and data, visit USDEC's Data Hub.

For more detailed information, as well as interactive charts and data, visit USDEC's Data Hub.

That said, we started to see some positive signal to close out the year. U.S. cheese exports recorded gains in November (+4%) and December (+1%), with solid volume increases to Mexico, China, Central America and the Caribbean.

U.S. NFDM/SMP shipments rose 1% in December, its first YOY increase since August 2023. December shipments to Southeast Asia jumped 23% (+3,634 MT) and volume to the Middle East/North Africa more than tripled (+1,868 MT). For Southeast Asia, it was the second straight monthly increase and an optimistic sign that demand in the No. 2 U.S. market is on the road to recovery.

Fluid milk and cream finished the year with four straight months of YOY gains. Volume rose 15% (+6 million liters) from September to December compared to the same period the previous year.

For a product-by-product breakdown of 2023 U.S. export performance, see below..png?width=554&height=300&name=Chart5%20(1662%20x%20900%20px).png)

NFDM/SMP

U.S. NFDM/SMP exports saw slight growth (+1%, 582 MT) in December—the first monthly increase since August. Overall NFDM/SMP exports for the year have been lackluster, with 2023 exports down 3% (-24,570 MT), but the decline only tells a portion of the story. U.S. NFDM exports to Mexico this year have boomed (+16%, 57,040 MT) although largely frontloaded in the year. NFDM exports to Mexico in H1 were up 39% (+62,842 MT). They eased in the back half of the year (-3%, -5,801 MT), but volumes were still large and up against strong exports in H2 of 2022. The Mexican economy has been very strong at a time when economies around the world mostly struggled. In addition to the strong economy, the peso has consistently strengthened against the dollar since Covid, making U.S. imports more attractive.

At the same time, exports to Southeast Asia suffered (-20%, -60,637 MT). 2023 for Southeast Asia was marked by high inflation and challenging domestic economics. Even with lower prices this past year, demand has been weaker. December did build on the slight growth seen in November with NFDM/SMP exports to the region up 23% (+3,634 MT) in the final month of the year.

Looking to 2024, we expect export volumes to Mexico to remain robust, but may not match the record volumes we saw in early 2023. In Southeast Asia, with easing inflation, lower NFDM/SMP prices and after a prolonged period of low import volumes, we expect demand to rebound in 2024. Overall U.S. NFDM/SMP exports should see some growth in the year ahead as the global economy continues to recover.

Cheese

While YOY U.S. cheese exports fell in 2023, it was (at 435,569 MT) the second highest volume we ever shipped in a single year. Volume was driven primarily by a 41% jump (+39,959 MT) in shredded cheese sales to meet foodservice demand, mostly to our top market, Mexico, but also to China. U.S. exports of shredded cheese to Mexico soared 162% (+39,131 MT) last year, while shipments of shredded cheese to China increased more than eight-fold (+5,612 MT).

However, those impressive gains were still insufficient to offset a decline in overall U.S. volume. Inflation-related consumption headwinds in Korea and Japan combined with heightened competition from the EU and New Zealand in South Korea to undercut U.S. cheese sales to both East Asian countries. U.S. cheese exports to Japan fell 15% (-7,155 MT) in 2023 and shipments to South Korea plunged 40% (-30,175 MT). Looking forward, more competitive pricing, European milk production struggling and expectations that Japanese and Korean demand for U.S. cheese may be poised to turn a corner paint a more hopeful picture for the coming year.

WPC80+

High-value U.S. WPC80+ exports crushed the previous volume record by more than 10,000 MT in 2023. Ongoing demand growth for high-protein foods in key markets coupled with lower WPC80+ prices in 2023 created a banner year for U.S. suppliers.

Gains were geographically broad-based. U.S. WPC80+ sales to Japan have risen now for nine consecutive years (+11%, +1,513 MT in 2023). The country took over as the top U.S. WPC80+ market from China in 2022, and despite erosion in YOY monthly growth at the end of 2023, Japan remains our No. 1 buyer. U.S. shipments to China rebounded last year (+47%, +4,520 MT) after higher prices weakened 2022 demand. And, driven by one of the biggest sports nutrition markets in the world, Brazil staked a claim as the fastest growing U.S. WPC80+ buyer in 2023. U.S. shipments of WPC80+ to Brazil are up now for four straight years and more than doubled to 8,462 MT last year. An even more encouraging sign is the ample room for growth. Demand for U.S. WPC80+rose in several developed and emerging markets last year, including Canada (+28%), Mexico (+35%) and India (+36%),while markets like South Korea and Southeast Asia are primed for demand rebounds.

Lower-protein whey (0404.10)

As we have noted in this column throughout the year, the U.S. low-protein whey export shortfall in 2023 is mostly about China. U.S. shipments of 0404.10 whey to China plunged 27% (-79,357 MT) as ongoing troubles in the nation’s pork industry severely curtailed demand. But China can’t be completely to blame for the decline. YOY U.S. export volume fell by a total of 125,165 MT in 2023, so the U.S. declined by more than 45,000 MT to other destinations.

Low-protein whey demand eroded across several geographies last year. In fact, U.S. shipments fell to eight of our top 10 markets in 2023. And exports declined for other suppliers as well. EU27+UK whey exports, for example, were down 10% (-62,429 MT) through November.

The challenges within China appear likely to persist, but our analysts are optimistic that demand in Southeast Asia, where a large portion of the dry whey is used for food applications, will rebound with an improved economic outlook. Given low-protein whey accounted for over 70% of the U.S. dairy’s export decline in 2023, any improvement in demand would put exports on better footing for 2024.

Lactose

YOY U.S. lactose exports fell 3% (-960 MT) in December, but overall lactose exports for the year were up 5% (+20,890 MT)—largely driven by gains to China. U.S. lactose exports to China in 2023 grew 23% (+26,813 MT). Likely supporting the increased exports were lower prices last year and increased usage for standardization within China—as detailed in our October write-up. U.S. lactose prices over the summer reached the lowest levels in nearly a decade. Prices have firmed since then, up 48% since July, which may impact export volumes moving into 2024, but prices are still roughly 30% below the average price since 2020.

Overall, U.S. lactose exports over the last few months have somewhat plateaued after robust growth in 2022 and much of 2023. Looking to 2024, it’s hard to get overly excited about strong growth as demand remains uninspiring.Learn more about global dairy markets:

-

Cheese rebounds in November, but overall U.S. dairy export volume declines

- U.S. dairy exports fall 7% in October

- U.S. export performance mixed in September

Subscribe to the U.S. Dairy Exporter Blog

The U.S. Dairy Export Council fosters collaborative industry partnerships with processors, trading companies and others to enhance global demand for U.S. dairy products and ingredients. USDEC is primarily supported by Dairy Management Inc. through the dairy farmer checkoff. How to republish this post.

-