.png)

-

U.S. dairy exporters told: ‘We don’t think real recovery is at hand.’

Unrelenting milk production growth and heavy inventories will continue to weigh on the global dairy market, forestalling a meaningful price recovery until at least mid-2016, according to Marc Beck, executive vice president of strategy and insights for the U.S. Dairy Export Council.

“We define ‘recovery’ as whole milk powder (WMP) prices returning to $3000/ton on a sustainable basis,” Beck told USDEC members today as he gave an analysis of global market conditions during a Midyear Member Webinar.

Oceania WMP prices are currently reported in a range of $1850-2200/ton, according to USDA’s Dairy Market News.

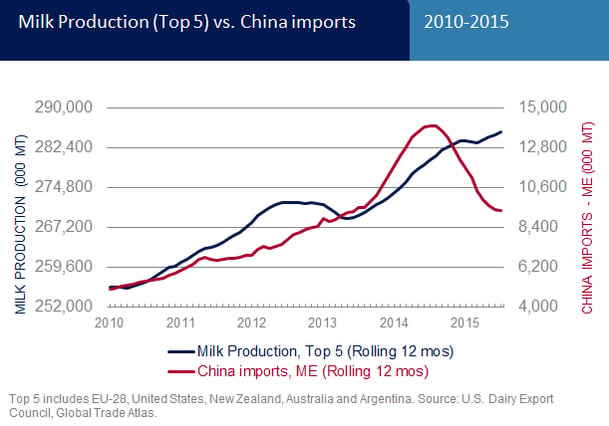

The three main drivers responsible for the 2015 milk surplus—increased milk production and reduced imports from China and Russia—have put an additional 13 million tons of milk on the world market over the last year, Beck explains.

“For the 12 months ending June 2015, milk production from the five major dairy exporters (the EU-28, New Zealand, United States, Australia and Argentina) was 5.6 million tons greater than the previous year. China’s imports were down about 4.6 million tons, milk equivalent, and Russia’s imports were down another 2.8 million tons, milk equivalent. So that’s a net supply increase of 13 million tons of milk, which the rest of the world has been unable to absorb.”

The outlook is for continued weakness as supply slowly rebalances.

“Milk production worldwide continues to increase,” Beck says. Output from the five major dairy exporters was up more than two percent in the second quarter. “We expect production to be up 1 to 2 percent in the second half of the year as well,” he adds.

Meanwhile, China’s own milk production is reportedly up about 4 percent this year. This excess milk is being diverted into powder, which is accumulating in inventory, Beck says. “No one knows for sure, but we’ve seen estimates that China could still be sitting on 300,000 to 400,000 tons of powder in inventory.

“China’s buying bubble of 2013-14 represented false demand,” Beck added. “During that time, China imports were way above trend, and way above milk production trends. Now those imports are below trend, but milk production continues to grow at trend.”

As China works down its holdings and exporters reduce their milk supply, the competitive environment for U.S. dairy exporters will remain very challenging—especially so because U.S. prices for cheese and butter are still at a premium to world price indicators.

“U.S. cheese is priced about 25 percent higher and U.S. butter is priced about 80 percent higher than what our competition is charging,” Beck said. “And, of course, historically U.S. exports have declined when U.S. prices are higher.”

As a result, U.S. export volumes are on track to decline this year for the first time since 2009, he predicted.

For additional data and analysis, see the latest issue of USDEC’s Global Dairy Market Outlook.

Subscribe to the U.S. Dairy Exporter Blog

The U.S. Dairy Export Council is primarily supported by Dairy Management Inc. through the dairy farmer checkoff that builds on collaborative industry partnerships with processors, trading companies and others to build global demand for U.S. dairy products.