.png)

-

Higher prices and increased cheese exports drove export value by 16% in the first month of the year.

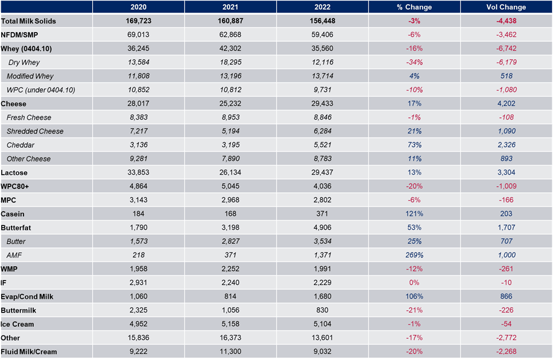

While January’s total export value grew 16% from a year ago (+$80.6 million to $586 million), the volume of dairy solids (MSE) declined by 3% (-4,438 MT MSE).

There were two key reasons for the divergence between volume and value. 1) A tighter global market raised unit values across the dairy complex. For example, the average price of nonfat dry milk/skim milk powder (NFDM/SMP) exports increased by $739 per metric ton (MT) from the previous January. Dry whey rose by $458/MT, and cheese increased by $68/MT. 2) The United States’ export portfolio increased in higher-per-unit-value products like cheese (volume up 17% year-over-year, +4,202 MT) and butterfat (+53%, +1,707 MT).

However, U.S. exports in its two biggest categories, NFDM/SMP and whey, lagged prior year volumes.

NFDM/SMP fell 6% (-3,462 MT) year-over-year caused by a 15% decline to Mexico (-3,587 MT), a 47% decline to South America (-2,544 MT) and a 41% fall to the Middle East/North Africa (-1,246 MT). Still, there were some bright spots for NFDM/SMP, with Southeast Asia up 9% (+2,117 MT) and exports to China doubling (+98%, +1,672 MT) despite logistics constraints shipping to East Asia.

But the major volume decline came from whey, which fell 16% (-6,742 MT) and which we’ll explore more in-depth in the section below.

U.S. dairy exports (month of January, data in metric tons)

We do want to reiterate before going into our major takeaways that it is important not to overstate one month of data. Overall, as we mentioned in our final report of 2021, we anticipate that export volume will likely be choppy in the first half of 2022 given supply chain difficulties, slower supply growth and tough year-over-year comparisons. And that is exactly what we saw in January.

With that in mind, here are our key takeaways from January’s data:

China’s Whey Demand for Feed Use Falling – William Loux

As mentioned above, the major driver behind the decline in dairy export volume is the decline in whey demand, particularly from China. In January, U.S. whey exports to China under HS Code 0404.10, which includes predominantly sweet whey and permeate, dropped by 41% (-9,163 MT). If that sounds familiar, it’s because December’s whey exports to China fell by 52% (-13,034 MT) and November’s fell by 21% (-4,093 MT). So, this decline is more than a one-month blip.

As for the reasons for the decline, we can point to two main factors: China’s falling demand and tight sweet whey supplies.

On the first point, most U.S. low-protein whey products shipped to China end up in the animal feed sector, since the market for whey permeates for food use—a key success in the U.S.-China Phase I agreement—remains a relatively new, albeit growing, market.

-Mar-08-2022-09-26-29-45-PM.jpg?width=554&name=Chart2%20(2)-Mar-08-2022-09-26-29-45-PM.jpg)

In that feed sector, the finances for China’s pig farmers have struggled of late. Pork prices have fallen precipitously from their African Swine Fever (ASF) highs as pork supply rebounded and anecdotes suggest that China’s consumers have switched to other animal proteins, namely chicken. Those lower prices have been compounded by elevated feed costs. The combination of lower prices and higher costs have eaten into China’s pork industry’s margins and thus dampened the incentives to expand production (and thus whey usage).

Beyond a rebalancing market in China, supply of sweet whey—which accounted for the majority of the decline in January—has been limited and expensive. Dry whey prices are at record highs, and U.S. dry whey production fell by 12% in the second half of 2021, caused by milk production slowing and demand for protein in the health and wellness sector pushing more whey towards WPC80 and WPI.

Looking ahead, both factors (China and supply) are likely to act as a persistent headwind to U.S. dairy export volume through the first quarter even as value is likely to stay strong.

Cheese Continues Growth Streak – Paul Rogers

U.S. cheese exports rose for the seventh consecutive month in January, increasing 17% year-over-year (+4,202 MT). Growth was more concentrated than it had been for the previous six months. A 74% jump in sales to Mexico (+3,223 MT) drove the gain, but Australia (+81%, +1,131 MT), the Caribbean (+27%, +369 MT) and Southeast Asia (+30%, +364 MT) also contributed.

On the positive side, it was the seventh straight month of year-over-year gains to Mexico and the 11th straight month to the Caribbean.

Other major U.S. cheese markets from 2021 took a breather in January. Year-over-year sales to the Middle East/North Africa fell 1% in January (after rising 39% in calendar-year 2021); exports to Central America fell 2% (after a 53% increase in 2021); and shipments to Japan fell 1% (after a 13% gain last year).

Those slowdowns might stem in part from foodservice uncertainty related to the omicron wave of the pandemic that began hitting importing nations in late November and is still making its way around the world.

In addition, the U.S. increase to Mexico should be looked at in context. The comparable volume the previous year was quite low. The United States shipped only 4,358 MT of cheese to Mexico in January 2021—the lowest volume of any month since November 2011. On the other hand, the 7,581 MT exported to Mexico in January 2021 marks the third-largest January volume ever.

More clarity on 2022 cheese demand should come in the months ahead, but the U.S. remains well-positioned from a production standpoint and in a favorable price position to meet overseas needs, with a geographic advantage to serve growing Latin American markets. Overall, sharply growing cheese exports should provide a major boost to U.S. export value.

Learn more about global dairy markets:

-

U.S. dairy exports set multiple records in 2021

-

NFDM/SMP, cheese and lactose led the way to double-digit export growth in November

-

Cheese, butterfat exports soar in October; milk powder, whey lag

-

Increases across the board keep U.S. dairy exports on pace for another record year

Subscribe to the U.S. Dairy Exporter Blog

The U.S. Dairy Export Council fosters collaborative industry partnerships with processors, trading companies and others to enhance global demand for U.S. dairy products and ingredients. USDEC is primarily supported by Dairy Management Inc. through the dairy farmer checkoff. How to republish this post.

-