.png)

-

The rebalancing of world dairy markets is still beyond the horizon.

The rebalancing of world dairy markets is still beyond the horizon.At the halfway point of the year, the global dairy markets are in their weakest position since 2009. Furthermore, with the slow rebalancing of world supply and demand, most observers are coming to the realization that the chance of the markets still rebounding this year is getting slimmer and slimmer. Analysts are pushing out their timetable for any kind of sustained improvement in prices to somewhere in 2016.

Though commodity prices are down significantly from a year ago—milk powder off more than 40 percent; cheese, butter and whey down 20-30 percent—global milk supply continues to expand. In the first quarter, global milk supply from the five major suppliers ((EU-28, United States, New Zealand, Australia and Argentina) was about flat. But in April and May production was up about 2 percent, with gains from every corner.

Right now the world doesn’t need that kind of milk production growth. In the first five months of the year, China imports (on a milk-equivalent basis) were down 38 percent from last year. That’s the equivalent of pushing back about 507,000 tons (1.1 billion lbs.) of milk per month. Powder stocks are still plentiful, and China’s milk production is reportedly up about 4 percent this year.

Meanwhile, Russia remains mostly out of the market indefinitely. Last week, Russia extended its ban on EU, Australian and U.S. dairy products for another year.

Other importers, such as Mexico, Southeast Asia and Japan, have bought aggressively, but they can’t make up for what China and Russia are leaving on the table. And with these early purchases, buyers are stocked up pretty well for months to come. Most are content to take a wait-and-see attitude toward buying ahead further. Now, we ease into the summer trading lull; we don’t expect to see buyers show more interest until September. By then they’ll have a better sense of New Zealand’s prospects as well, and whether the El Niño is having any impact on production.

Other fundamental indicators:

- EU-28 milk deliveries in April are estimated at 13.2 million tons, up 2.0 percent from the extraordinary levels of last year. Among key countries in April: Ireland +11.3 percent; Netherlands +1.7 percent; Germany -1.4 percent; France -1.0 percent.

- New Zealand milk production was up 8.5 percent in April, while Australia posted a 2.9 percent gain. Pastures in New Zealand are in good condition for the start of next season.

- U.S. milk production continues to expand. May output was 8.3 million tons, up 1.4 percent from prior year.

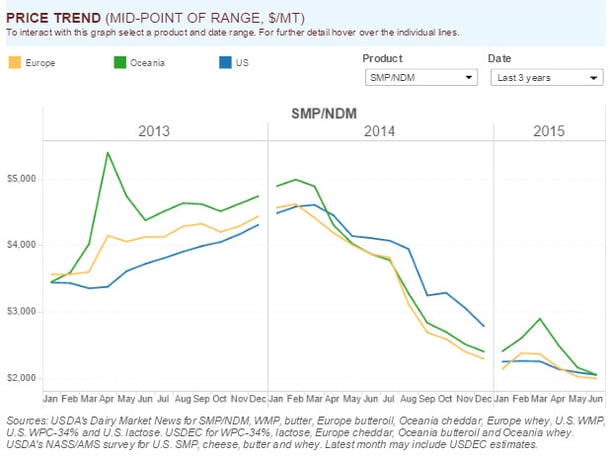

- In the first five months of the year, China imported 223,137 tons of WMP, down 54 percent from the exceptional volumes bought last year, though about the same as the 2011-13 average for the same time period. SMP imports were down 31 percent and whey products were down 4 percent from a year ago.

- NZX futures continue to reflect bearish sentiments. WMP futures average $2350/ton to December.

- The GlobalDairyTrade (GDT) Price Index dropped for the seventh event in a row at the June 16 auction, falling 1.3 percent to an average winning price of $2,409/ton. The Index has dropped 29 percent since early March and now sits at its lowest level since August 2009. WMP was down 0.1 percent to an average winning price of $2,327/ton, SMP was off 0.2 percent to $1,978/ton and AMF was down 8.9 percent to $2,814/ton.

To hear me discuss the global dairy market outlook with Bill Baker on Dairyline, a DairyBusiness radio show, click the audio bar below.

The U.S. Dairy Export Council is primarily supported by Dairy Management Inc. through the dairy farmer checkoff that builds on collaborative industry partnerships with processors, trading companies and others to build global demand for U.S. dairy products.